Importance of Investing

- Mangesh

- Aug 25, 2019

- 5 min read

Updated: Sep 25, 2019

When you invest, you are committing your money or other resource in the expectation of some future benefit. A college education can be considered as an investment because you invest your time (A Resource) in hope of earning a degree and secure a good job in the future. Here you are investing your time and taking efforts to get returns as knowledge and skills to fetch a job. Anyone can start making an investment (even with small capital) and start building financial assets.

Following are the few reasons that will make you understand why starting to invest your money is not a bad idea !!

Why should I Invest ?

Beating the Inflation

Suppose you decide to keep all of your money in cash and not invest at all, over the time actual worth of the money will go down due to inflation. Resources that you can buy today are more than you can buy in future as demand keeps increasing and prices goes up. Hence, at least to keep worth of your money intact you should invest your money, where returns are higher or equal to Inflation.

Putting your idle Money to Work

Everyone is familiar about concept of working for money. Most of people spend their entire life working for money just to find out that hardly any money if left after years working for it. There is secret very few people know and even fewer practice is to make your money work for you. Initially you have to work for money and eventually your money starts working for you and you will no longer have to work. Seems impossible !! it is actually quite plausible and can happen if you use magic of compounding (Refer my blog on Compounding).

Fulfill your Dreams

You must have dreamed about buying a fancy car, Luxurious house or going on foreign vacations. But for most of people these remain dreams only as they think they are never able to save enough. Secret is not whether you can save enough, but it is whether you can invest enough of your saving at a rate which can fulfill your Dreams !!

Saving for Retirement

Everyone has to retire at some point of time in their life, if you don’t have sufficient fund at the time of retirement, your life can be pretty miserable. With the help of investments, you can live comfortable life even after retirement or take an early retirement.

There are several options available to Invest but, first as an investor you have to decide which option or Asset class is most suitable for you. Each class of investment has different types of risk and Reward.

There are several factors that you have to consider while making an Investment

1) What is your Goal

Each investor can have different goal. A person who is going to retire in next few years might want to park his money into safer options where he is able to generate continuous cash flow for his needs while keeping principal amount safe like investing in Systematic Withdrawal plan of Bonds. While a young investor with lesser responsibilities can have higher risk appetite and can invest in slightly riskier options where he is able to generate wealth in next few years.

2) Time period of Investment

There are some investment options which are highly illiquid i.e. it may take few years and right time to sell them, like real estate. There are cyclical asset classes where your money can grow significantly over period of time only if you stay invested across few cycles like stock market. Few options give you ability to withdraw your money in no time and cushion of safety like money market instruments.

Where Should I Invest ?

There are several asset classes each having particular risk and return characteristics. Following are some of the most popular asset classes

1) Fixed Income Instruments

Fixed Income instrument is the oldest and one of the most trusted form of investment among Indian Investors. This asset class has very low risk to the investors and returns are paid as Interest to the investors. After term of deposit or maturity period principal amount along with accumulated interest is paid to Investor.

Typical Fixed Income Instruments are as follows –

Fixed/Recurring Deposits offered by banks

Public Provident Funds (PPF)

Money market Instruments like Commercial Papers, Certificate of Deposits (CD’s)

Bonds Issued by Government of India

Bonds Issued by Government Agencies like HUDCO (Housing and Urban Development Corporation), NHAI (National Highway Authorities of India)

Bonds Issued by Corporate companies

Typical returns from Fixed Income Instruments range from 8 to 11 %

2) Commodities

Commodities can be anything like Goods, Products, Precious metals like Gold and Silver. Here price can vary as per Supply and Demand.

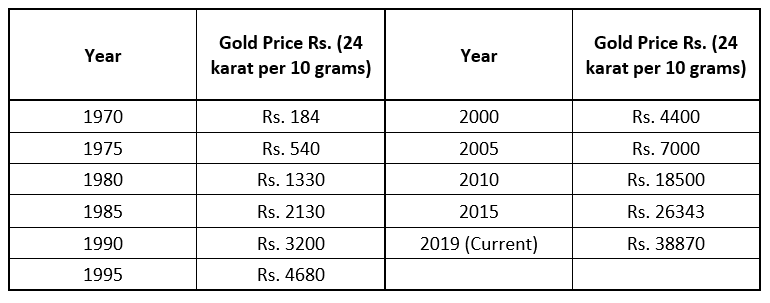

Buying gold is also a very popular investment option in India. Gold is not only treated as a investment option but it is also considered auspicious and symbol of social status. Up to 25% of the world’s gold is consumed in India in form of Jewellery, Bars or Coins.

Commodity market is cyclical in nature and returns can vary drastically. Following are the historical returns on the Gold

Going by the above data historical returns from the gold are as follows –

3) Real Estate

Real estate is an asset class that involves buying plots, apartments, commercial buildings, industrial areas etc.

Investment in real estate generates returns in two forms

1) Rental Income

2) Capital Appreciation

Real estate investment is considered a great investment option as it can generate passive income and also price appreciation happens over a long-time frame.

But it is highly illiquid asset and requires large amount of money to be invested in one go. Investing in real estate is a complex process which involves finding a right property to buy which has potential to appreciate in value in next few years, paying several taxes like GST, Stamp Duty, Registration charges, Verification and preparation of several legal documents. Real estate investment has costs involved like maintenance cost, potential income gaps if there are no tenants. Also selling of real estate is a time-consuming task and may not fetch you money when you need it.

There is no official metric to measure returns generated in real estate. Returns can vary greatly based on Location, Future growth prospects in the surrounding area, Government policies, Rental yield etc.

Real estate investment mostly uses leverage i.e. borrowing money for investment. As case with any leverage a smart investment can make you millionaire in few years while it also has a potential to tie up your significant capital for long period while you are paying huge interest on borrowed capital. This asset class has potential to deliver high returns unlike Fixed income or Gold. But it also needs huge capital, time as well as ability to use leverage to buy at correct time and place.

4) Equity

Investment in equity involves buying shares of companies listed on stock exchange. Buying shares of a company represents equity ownership in the company. Equity investors buys shares of a company with an expectation that they will rise in value in form of capital gains and also generate dividend income. Investment in equity does not guarantee any fix returns but as a trade off returns from equity can be highly attractive. Indian equities have generated close to 14-16 % CAGR returns over the past few decades. But having a good portfolio with proper risk management can allow you to earn higher returns in excess of 20% in long term.

For example,

SENSEX

If person invested Rs 780 in index during 1990 then amount would have compounded to Rs 39000 in 2019

BAJAJ FINANCE

Rs. 5 invested in Bajaj Finance in 2002 would have compounded to Rs 3967 in 2019, whooping returns of 64000%

There are similar growth stories of several Indian companies but one has to asses the risk and make a wise decision to invest in right companies as there can be lot of volatility in the short term. Equity is a risky but highly rewarding investment vehicle.

Tax benefits are also attractive in case of equity investing. If equity shares are held for more than one year (365 Days) then any capital gains above 1 lakh are taxed at 10% only (LTCG Tax) which is much lower than tax rates on other investment instruments.

Comments